When you’re starting with basic investing for beginners in the U.S., you’ll often hear phrases like “the magic of compounding” or “interest on interest.” This isn’t just financial jargon; it’s the fundamental principle that drives long-term wealth creation. Understanding compound interest is arguably the single most important concept for new investors.

Often attributed to Albert Einstein as “the eighth wonder of the world,” compound interest allows your money to grow at an accelerating rate, turning small, consistent contributions into substantial sums over time.

What is Compound Interest?

In simple terms, compound interest is the interest you earn not only on your original investment (your principal) but also on the accumulated interest from previous periods. It’s a snowball effect: your money makes money, and then that money starts making money too.

Let’s illustrate with an example in the U.S. context:

Imagine you invest $1,000 in a fund that earns an average annual return of 7% (a reasonable historical average for the U.S. stock market after inflation).

- Year 1: You start with $1,000. You earn 7% interest ($70). Your new balance is $1,070.

- Year 2: Now, you earn 7% interest not just on your original $1,000, but on the entire $1,070. So, you earn $74.90 ($1,070 x 0.07). Your new balance is $1,144.90.

- Year 3: You earn 7% on $1,144.90, which is $80.14. Your balance grows to $1,225.04.

Notice how the amount of interest you earn increases each year, even though the interest rate remains the same? That’s the power of compounding. The interest earned in previous periods is added to your principal, and then the next period’s interest is calculated on that larger sum.

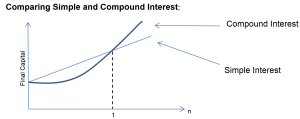

Compound Interest vs. Simple Interest

To truly grasp compounding, it helps to compare it to simple interest:

- Simple Interest: Interest is calculated only on the original principal amount. If you had that same $1,000 at 7% simple interest for 3 years, you’d earn $70 each year, for a total of $210, ending with $1,210.

- Compound Interest: Interest is calculated on the principal and the accumulated interest. As seen in the example above, you’d end up with $1,225.04. While the difference seems small over three years, it becomes massive over decades.

For investors, compound interest is almost always the goal. Simple interest is more common in certain types of loans.

Key Factors Influencing Compound Interest Growth

Several factors impact how quickly your money compounds:

- Time: This is arguably the most crucial factor. The longer your money is invested, the more time it has to compound, and the more dramatic the growth becomes. Starting early, even with small amounts, vastly outperforms starting later with larger sums.

- Interest Rate (or Rate of Return): A higher interest rate means your money grows faster. The average annual return of the U.S. stock market (as measured by the S&P 500 index) has been approximately 10% over the last century before inflation. While not guaranteed, investing in growth-oriented assets like stocks (through diversified funds) generally offers higher compounding potential than traditional savings accounts.

- Compounding Frequency: How often is the interest calculated and added to your principal? It can be annually, semi-annually, quarterly, monthly, or even daily. The more frequently it compounds, the faster your money grows, as interest is being added back into the principal more often. Investment accounts typically compound regularly.

- Additional Contributions: While compound interest works on its own, adding more money to your investment regularly accelerates the process even further. This is why consistent investing through strategies like dollar-cost averaging is so powerful.

The “Rule of 72”: A Quick Estimate

For a quick estimate of how long it takes for an investment to double in value due to compounding, use the Rule of 72. Simply divide 72 by your annual rate of return (interest rate).

- If you earn 8% annually, your money will roughly double in 9 years (72 / 8 = 9).

- If you earn 4% annually, it will take about 18 years (72 / 4 = 18).

This rule clearly illustrates how higher rates of return significantly shorten the time it takes for your wealth to grow.

Why Understanding Compound Interest is Vital for U.S. Beginners

- Empowers Early Investing: Knowing how powerfully compounding works motivates you to start investing as soon as possible, even with small amounts.

- Encourages Patience: It teaches you that patience is rewarded in investing. Riding out short-term market fluctuations is easier when you understand the long-term compounding potential.

- Highlights Consistent Saving: It reinforces the importance of regularly contributing to your investments to continuously fuel the compounding machine.

- Reveals the Cost of Debt: Compound interest also works in reverse for loans, especially high-interest debt like credit cards. Understanding this can motivate you to pay off debt quickly to avoid exponential growth in what you owe.

Conclusion

For beginners in the U.S., understanding compound interest is not just an academic exercise; it’s the key to unlocking your financial potential. It demonstrates that you don’t need to be a financial genius or have a massive starting sum to build substantial wealth.

By simply starting early, consistently investing in assets that offer reasonable rates of return (like diversified stock market funds), and allowing time to work its magic, compound interest will become your most powerful ally in achieving your long-term financial goals, from retirement security to a comfortable future. Embrace its power, and watch your money grow.